Issue 8 | AOFM Investor Insights | August 2021 | PDF

The AOFM recently conducted around 50 virtual meetings with key offshore investors as part of a regular post-Budget engagement program. These took place over the period 13 July-5 August and provided investors with updates of the AOFM’s issuance outlook, the main considerations likely to impact operations, and context to the Budget forecasts. It was also an opportunity for investors to give updates on how they are viewing the AGS market, including to ask questions or seek clarification of AOFM issuance announcements and other government policy including RBA activity.

Investors were provided with a chart pack. The AOFM also provided a summary of the Australian Government’s main climate change commitments, policies, and programs.

A summary of investors contacted by type and geography is below.

Table 1:

| Investor Type | |

| Fund Manager | 33% |

| Central Bank/Sovereign Wealth Fund | 29% |

| Hedge Fund | 23% |

| Insurer/Life Office | 6% |

| Pension Fund | 4% |

| Bank Balance Sheet | 4% |

Table 2:

| Geography | |

| Asia ex-Japan | 33% |

| UK | 25% |

| Americas | 23% |

| Europe | 19% |

Background

In addition to the Budget 2021-22 (released 11 May 2021), there were several other releases by the AOFM and the RBA, which provided further information and generated issues for discussion. They included:

- CEO speech to the Australia Business Economists luncheon (8 June 2021) - Last year: Not just one to remember, but one to learn from

- AOFM issuance program update (2 July 2021)

- RBA statement of monetary policy decision (6 July 2021)

The main topics of the meetings covered:

- A fiscal and economic update – including consideration of assumptions in the Budget forecasts in the context of emerging upside and downside risks (given the period during which the engagements were conducted).

- AOFM issuance plans for Treasury Bonds, Treasury Notes and Treasury Indexed Bonds.

- The influence of the RBA’s bond purchase program and yield curve control operations on AOFM issuance (and some feedback from investors on AGS demand and liquidity).

- How offshore investors perceive AGS market relative value against other sovereign bond markets.

- The relevance of ESG considerations to sovereign bond investment decisions.

Fiscal and economic update

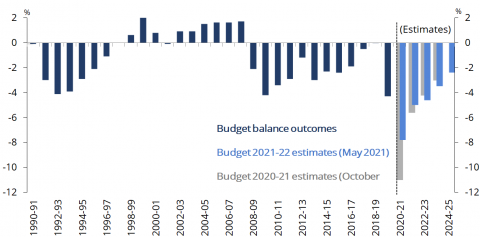

Investors were generally positive on the outlook for the Australian economy. Chart 1. (below) highlighted the improvement in the budget position and forward estimate projections as compared to MYEFO (December 2020) and Budget 2020-21 (October 2020).

Chart 1: Budget balance outcomes and forecasts

As the meetings progressed discussions focussed on both upside and downside fiscal risk (the latter being brought about by a resurgence of Covid infections due to the spread of the delta variant and lockdowns in some parts of Australia including the two largest cities - Sydney and Melbourne).

Questions from investors:

- What is the impact of lockdowns in the major cities on Budget forecasts and AOFM issuance plans?

- Why is the vaccination rate in Australia relatively low, and what is the assumptions for vaccination levels in the Budget? What are the challenges to achieving the vaccination rollout?

- What is the expected timing for the Australian international border to reopen?

- Would a slowdown in population growth lead to a tighter labour market and upward pressure on inflation and wages?

- What are the assumptions for the price of key commodities, especially iron ore? Why are they so conservative?

- Do Budget forecasts factor in a deteriorating trade relationship with China?

AOFM messaging

- The iron ore price is assumed to decrease to a long-term ‘equilibrium’ price of US$55 a tonne by March 2022 (in July 2021 the average price exceeded US$200, although it declined in August from its highs). It is estimated that every US$10 increase over US$55 adds around A$1.3 billion of additional tax revenue per year. This presents a potential source of upside risk to Budget forecasts.

- The Budget forecasts assume a completed population-wide vaccination program by the end of 2021 – given the recent increase in vaccination rates across Australia and increase to supply negotiated by the Government, this assumption remains credible.

- Budget forecasts assume that there will be a gradual return of migrants and international students from mid-2022.

- The assumptions most at risk is that there would be no extended state border restrictions, and that although there would be localised outbreaks of COVID-19, they would be contained. As the situation in Sydney persists (and possibly worsens) and there are material risks to other major centres (for example Melbourne) this will require unbudgeted fiscal support and create a deterioration in tax revenues. There are outlay contingencies in the Budget but not to cover widespread extended lockdowns. The Commonwealth and the states are cost sharing fiscal support.

- There are no explicit assumptions in the budget for declining trade with China, although arguably a conservative forecast for nominal GDP in the Budget driven by a forecast decline in the terms of trade provides some level of ‘cushion’. Notably, the latest ABS trade data shows that exports in key commodities remains at or above record levels.

AOFM issuance update

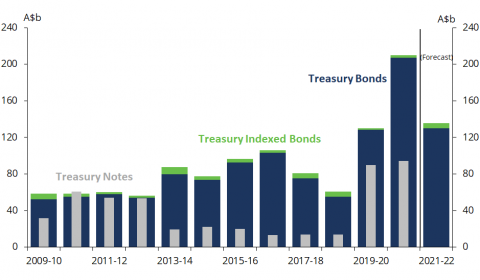

Announced Treasury Bond issuance for 2021-22 is $130 billion (see chart 2), which could be adjusted: (1) downwards if ongoing revenue strength observed from the end of 2020-21 continues into 2021-22 or (2) upwards if COVID related lockdowns persist for an extended period. By the conclusion of the meetings the AOFM view was that these risks were ‘balanced’. The Budget strength evident prior to widespread lockdowns will, at least partially, offset any deterioration in the Budget that could emerge during 2021-22.

Chart 2: Issuance of Australian Government Securities

Ultra-long end Liquidity

A consistent theme from investors participating in the ultra-long end of the Treasury Bond curve is its attractiveness on a relative value basis, both according to yield spread (against other sovereigns) and relative to economic fundamentals. However, it continues to exhibit low liquidity. Investors were generally supportive of AOFM’s plans to move way from using tap syndications in the long end with a switch to relying on smaller tenders on a more frequent basis. Questions included:

- Would the AOFM look to increase the average tenor of issuance to take advantage of relatively low outright yields?

- What are the expected tender sizes and how often will the AOFM issue in the long end?

- Would the AOFM provide longer than usual notice of ultra-long end issuance?

- What will the next maturities be in the long end?

AOFM messaging:

It’s likely that the average tenor of issuance overall will be slightly lower than last year, in part because there is no need to issue another new 30-year benchmark for a few years. The bulk of issuance will be into the most liquid parts of the curve between, and including, the three[1] and ten-year futures baskets. The reason for moving to small tenders in the ultra-long end is to promote more consistent liquidity. The frequency of the tenders will take account of market demand, and issuance will be announced at the same time as all weekly tenders on the preceding Friday (but the tenders will probably be held mid-week).

The pattern of new maturities from last year wouldn’t be expected to be repeated this year since the issuance program for this year is much smaller and there are no maturity ‘gaps’ to fill, except beyond the 10-year futures basket. One new 2043 or 2044 maturity between the 2041 and 2047 is planned to support the 20-year futures contract. It may be issued in either the second half of this or next financial year (the next issuance update is post MYEFO – that is in January 2022).

RBA bond purchase program

Investors asked about the RBA bond purchasing program and its impact on AGS market liquidity, and whether it affects AOFM issuance operations.

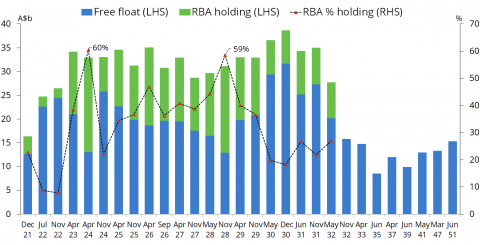

Chart 3: Treasury Bonds on issue – RBA holdings and ‘free float’

Investors noted that liquidity between the three and ten-year futures baskets was still good despite RBA holdings approaching 30% of the market. Liquidity was consistently assessed as challenged in the short end. Some noted from their experience in other sovereign markets, such as Japan and Sweden, that overall liquidity becomes noticeably lower when central bank holdings reach around 40% of bonds outstanding. How investors perceive liquidity depends on both the area of the curve they hold and their frequency of trading, noting that all markets have slightly different features. For example, many central banks hold relatively illiquid short-dated bonds, but if they are not trading frequently then they are less concerned.

On the other hand, some hedge funds reported that their activity in AGS had declined since the commencement of RBA bond purchasing. Hedge fund strategies rely on exploiting pricing volatility along the curve. Several hedge funds noted that RBA bond buying had significantly reduced volatility in short-dated bonds and cheapened three and ten-year futures contracts (relative to the underlying bonds), making them a less effective trading strategy when funding with repo. Some reported that RBA buying in the mid-curve had reduced the incentive for banks to make tight two-way prices and that this could limit participation in the mid-part of the curve.

Most hedge funds reported that access to repo and pricing of repo was not a limiting factor in their participation in the market – although some assess spreads and pricing as remaining wide.

AOFM messaging

AOFM is viewing line sizes on a ‘free float’ basis, that is the amount outstanding excluding what the RBA holds. This means there is capacity to tap these lines in response to signs of poor liquidity and that the AOFM can easily continue to issue into them without consideration for gross amounts outstanding even as the individual lines grow.

The AOFM has decided not to issue into any bond lines that form part of the RBA’s yield curve control operations, and the RBA has not been offering to buy a bond-line in the week following the week in which the AOFM issues it.

Offshore Investor Demand for AGS

Investors were interested in discussing trends in offshore demand for AGS. Questions included:

- What trends is the AOFM seeing in investor demand?

- Is the recent decline in offshore holdings of AGS due to RBA buying or a decrease in offshore demand more generally?

- What are the trends in Japanese demand for AGS – are they buying or selling AGS?

AOFM messaging

- Overall, we have not seen an appreciable withdrawal of investor support from offshore, although a decline in the use of repo by non-residents would indicate that hedge funds are currently less active in the market than they were last year.

- As the RBA becomes a larger holder of the AGS market, that will naturally substitute for a range of AGS investor activity but to date the AOFM is not aware of any structural change to the underlying AGS investor base.

- The one investor group that has noticeably reduced holdings since RBA bond purchasing commenced, however, are domestic bank balance sheets.

- Japanese investors were significant buyers of Australian government bonds in 2020. Data from the Japan Ministry of Finance (MoF) shows there has been some net selling (AGS and semi-government bonds combined) in the first half of 2021, although the rolling 12-month accumulation remains positive. Secondary market AGS turnover provided by market makers confirms this.

Treasury Notes

There was interest in Treasury Notes, despite very low yields. Although a minority of offshore investors spoken to are current Treasury Notes holders, they are across investor types – central banks, fund managers, and insurers. For some, Treasury Notes are a useful liquidity tool, while others can earn a pickup to US T-Bills after currency hedging.

Questions from Investors:

- What are AOFM issuance plans, and would there be a minimum amount outstanding?

- Would AOFM look to take advantage of low (sometimes negative yields) and issue more?

- Would AOFM issue longer dated Treasury Note lines out to 9-12 months?

- Is there a link between Treasury Notes issuance and changes in the funding task, AOFM cash holdings, and the nominal bond program?

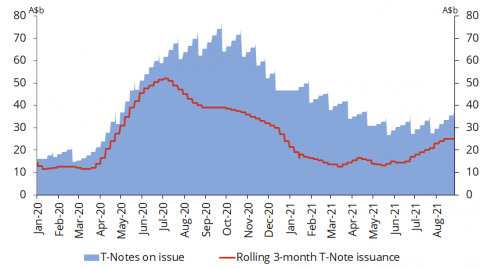

Chart 4: Treasury Notes on issue and rolling 3-month issuance

AOFM messaging

- An annual issuance forecast is not available since Treasury Notes are primarily a within year cash management tool and the extent of use depends on the timing of receipts and expenditures that are not known with certainty. There are certainly parts of the cash portfolio cycle where they will be used noticeably more heavily.

- Treasury Notes proved to be highly effective as an available source of liquidity when they were needed in 2020.

- AOFM plans to be a regular issuer of Treasury Notes. Amounts on issue will vary over the course of the year, however a minimum amount will be maintained around where levels were in early June 2021.

- At times when there are high volumes of Treasury Notes on issue there will be longer dated Treasury Notes.

- No specific interpretation on the budget position can be made from Treasury Note issuance – the annual nominal bond program would typically be adjusted to account for a marked change to the funding task.

Treasury Indexed Bonds

Investors noted that Australian break-even inflation (BEI) rates seem relatively cheap compared to many inflation markets, including the US and the UK. Some investors consider that the RBA stance on only adjusting monetary policy settings after inflation is sustainably within their 2-3% target should be supportive for TIBs. A limiting factor for many to participate is the poorer liquidity of the TIB market compared to Treasury Bonds.

The forthcoming November 2032 syndication would attract attention as a possible entry point into the market. For some investors TIBs forms part of a specific mandate, or are included in their global benchmark, while for others TIB holdings are more opportunistic.

Questions from Investors:

- Is the choice of maturity and timing of the Nov-32 syndication in response to investor feedback or part of a regular program?

- What would AOFM expect the size of the deal to be?

- How will the buyback level of the February-2022 be determined?

AOFM messaging

- The AOFM’s objective is to support and maintain a functioning linker market, primarily through regular tenders. TIBs play no meaningful role in the Budget financing task simply because the market is too small to absorb large amounts of issuance.

- The November 2032 is primarily being issued to maintain a 10-year benchmark, which market participants consider to be an important pricing point. It will be a very procedural transaction.

- The size of the deal will be determined by investor demand and set at a level where the bond is most likely to perform in the secondary market. Careful consideration will be given to the composition of the book in allocating the final volume.

- Consistent with past practice the AOFM will consider a buyback of the 2022 line. For many investors bonds less than one year in maturity are not included in their benchmark. The buyback may free up cash for some investors to participate in the deal. The buyback price would be based on the prevailing market rate.

Update for the November 2032 syndication

The new November 2032 TIB was priced on 24 August 2021. The final print size of $3.25 billion did not create notable surprise. Around 20 per cent was allocated to offshore investors, demonstrating that the TIB investor base remains primarily domestic focussed. Around 71% of the deal was allocated to fund managers including asset managers, insurers, and pension funds. In conjunction with the deal the AOFM repurchased $1.72 billion of the February 2022 bond line (about 25% of the total amount on issue).

ESG considerations

Over the last few years both domestic and offshore investors have increasingly been seeking to engage with the AOFM on ESG issues.

The AOFM included an information pack on details of Australia’s key environment and climate related commitments and the Government agencies and organisations responsible for collating the associated data on progress toward commitments. Feedback indicated the pack was very useful, and it generally provided a platform for further discussion on ESG issues and investor demand.

Around a third of the meetings included an ESG related discussion. Many investors have specific green bond mandates and would have demand for a green bond if the AOFM were to issue them. The types of investors with green bond mandates include central banks, sovereign wealth funds, fund managers, pension funds and insurers. Some investors are more focused on the ESG credentials of the sovereign as an issuer rather than on a green bond per se. An increasing number of investors are signatories to climate related investor agreements in which they are required to report on the overall ‘climate performance’ of their portfolios. However, feedback to date suggests these agreements are more relevant for investments in equities, and corporate bonds than sovereign debt; but increasing attention is being placed on sovereigns as issuers.

AOFM messaging

- The AOFM is closely monitoring developments in ESG issues and green finance, from both an issuer and investor perspective, and is open to engaging with investors on this topic.

- A decision to issue a green bond would need government approval and could not be made by the AOFM alone.

Summary

The AOFM commenced an annual program of virtual invertor meetings several years ago and this formed a well-tested platform to meet the challenges emerging last year (and continuing on the basis of restricted travel opportunities). Consistent feedback is that investors, and the banks who help to organise the meetings, find them to be valuable as a means of engagement on key issues regarding the AGS market and planned issuance. Future engagement plans for the remainder of 2021, include a round of meetings with domestic investors as well as a focus on key Japanese investors.