Issue 4 | AOFM Investor Insights | June 2020 | PDF

Recently the AOFM conducted around 80 calls with key offshore and domestic investors. The purpose of the calls was to provide a preliminary investor update focusing on:

- AOFM announcements regarding changes to issuance resulting from the Government’s fiscal response to the emerging pandemic situation;

- outlining the behaviour investors can expect from AOFM as an issuer over the coming 12-18 months; and

- gauging investor views of the AGS market since the market dislocation arising in mid-March.

A summary of investors contacted by type and geography is below.

Table 1: Investor Type

| Investor Type | % |

|---|---|

| Fund Manager | 45 |

| Central Bank/ Sovereign Wealth Fund | 22 |

| Hedge Fund | 13 |

| Bank Balance Sheet | 10 |

| Pension Fund | 7 |

| Insurer/ Life Office | 3 |

| Total | 100 |

Table 2: Geography

| Geography | % |

|---|---|

| Australia | 31 |

| Asia ex-Japan | 25 |

| United Kingdom | 13 |

| Europe | 12 |

| Japan | 10 |

| Americas | 9 |

| Total | 100 |

Summary

The investor calls began in mid-April, just as the AGS market was beginning to show signs of meaningful recovery following the significant dislocation erupting in mid-March. It was a productive time to provide a program update because: (1) gauging the change in mood and experience from investors during the market recovery was enlightening; and (2) highlighting key messages helped give investors a far better understanding of what was happening in the AGS market over a range of key issues. Broadly speaking investors indicated a positive assessment of: Australia's overall approach to its fiscal response; AOFM’s efforts to communicate with and update the market; and the RBA’s monetary policy and related market support operations.

Recurring issues discussed were:

- how the Government’s fiscal stimulus measures would operate and the potential for downside program cost risks;

- market conditions in general including AGS liquidity experiences during and after the market dislocation;

- expected changes to the AOFM’s term issuance program for 2019-20 and how this interacted with the strong build-up in Treasury Note issuance; and

- how the RBA’s market operations could be interpreted, and the impact they were having on the market.

Strength of the Government’s balance sheet

Some offshore investors raised the potential for a sovereign rating downgrade given the indicated volume of issuance required to fund the fiscal response and the expected Budget deterioration. Of those that raised the issue, there was no indication from them individually that a downgrade would impact demand for AGS.

AOFM’s message to investors

The Australian Government entered the pandemic crisis with a strong balance sheet and underlying fiscal position (and outlook). Post-crisis, the balance sheet position will continue to exhibit relatively low net debt by global standards. Rating agency reactions are supporting this assessment.

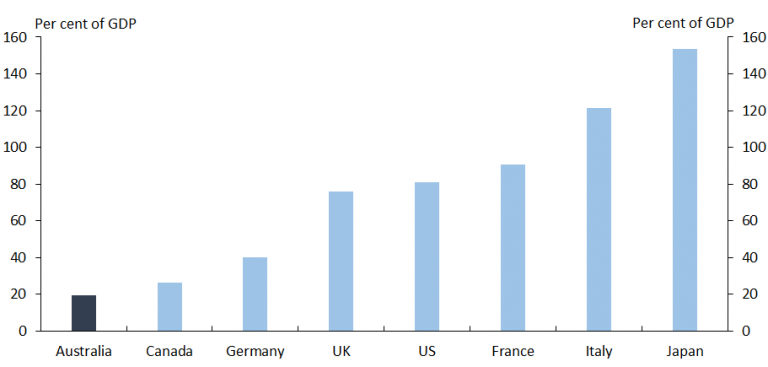

Chart 1. 2019-20 net debt to GDP forecasts prior to COVID-19

Australian Government fiscal stimulus measures

While domestic investors had a good understanding of the Government's stimulus package, offshore investors sought clarification on specific measures. Questions focused on the JobKeeper package in particular (and the potential for downside risk to the costs of the program), and support to business via the various programs that would use the financial system as the basis for delivery. Questions included:

- if the duration of JobKeeper would be extended, eligibility, and the level of support;

- the level of support to be provided by the Government to small and medium-sized enterprises and how the loan guarantees by the Government would work; and

- how the RBA’s balance sheet would be used to support businesses.

Liquidity and market conditions

During the initial calls in April, investors were concerned with market liquidity and how the RBA’s market support operations could be interpreted. Investors were assessing what the impact would be on markets globally of the cumulative fiscal measures being announced around the world, not just in Australia. Some observations from these discussions were:

- Domestic fund managers and super funds had caused outflows from fixed income due to rebalancing and redemptions. Fund managers who needed to access cash sold AGS, as it was one of the very few asset classes where liquidity was available.

- Some offshore investors, especially those using leverage (hedge funds), had sold significant amounts of AGS due to reduced repo access, and also to stem losses after bonds sold off.

- Investors reported liquidity as being ‘non-existent’ in the linker market and very poor in ultra-long maturities.

- Over the course of the calls confidence was returning, associated with an increase in duration risk appetite coming back to the market.

- The new November 2024 syndicated issue was noted as highly successful (good pricing, appropriate concession, functional deal size) and this generated more confidence in market recovery (some investors at that point also signalled interest in a new longer maturity).

- The new December 2030 syndication was also seen as highly successful (good pricing, appropriate concession, functional deal size).

- Hedge funds remained very interested and focused on Australian Government Bonds with a number expressing concern about market liquidity and access to repo funding. However, toward the end of the call program, these views had abated noticeably.

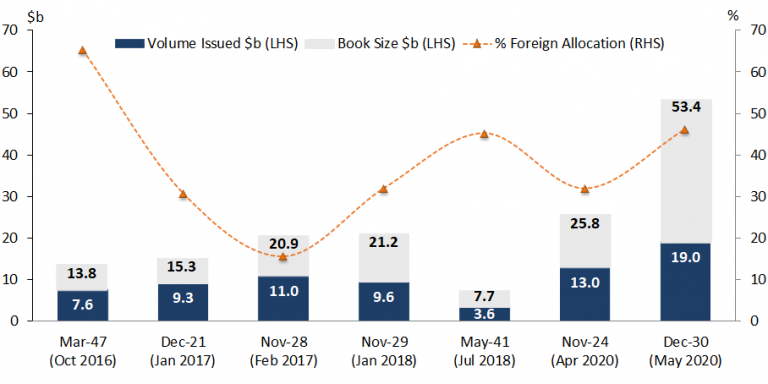

Chart 2 shows relatively strong demand and offshore interest in the December 2030 syndication and highlights the support from offshore investors for long bond syndications.

Chart 2. Treasury Bond syndications

RBA operations

Investors were particularly interested in the RBA’s AGS market operations and how to distinguish yield curve control and 'market-functioning’ bond purchases. Common questions and themes included:

- Comparisons with other central banks’ approach to quantitative easing – why is the RBA not providing volume targets.

- Do you expect the RBA to buy across the curve out into ultra-long maturities? Could the operations be expected to include inflation linked bonds?

- What is the nature and frequency of communication between RBA and AOFM?

- Will the RBA buy AGS directly from the AOFM rather than through the secondary market?

- Would the RBA be able to maintain its ‘taper’ in terms of it slowing down the rate of bond purchases?

Investors noted that the AGS yield curve was relatively steep. Some argued that this was predominantly a result of the RBA not buying across the curve. A number expressed concern that this signalled a lack of support for the AGS yield curve and would result in prolonged volatility and lack of liquidity. Others, especially offshore, saw opportunities in AGS based on: comparative yields to other sovereigns; recent widening of AU/US bond spreads; the level and resilience of the currency; and some improvements in FX hedge costs. For many investors, the RBA being less active in the government bond market compared to other sovereigns was viewed favourably as this reflected less chance of ‘distortion’ in the AGS market.

AOFM messaging

- AOFM issuance decisions are independent of RBA monetary policy operations.

- The RBA buys bonds in the secondary market, rather than directly from the AOFM because the former reflect market functioning considerations (or are tied directly to monetary policy objectives), while the latter would represent direct monetisation of government debt.

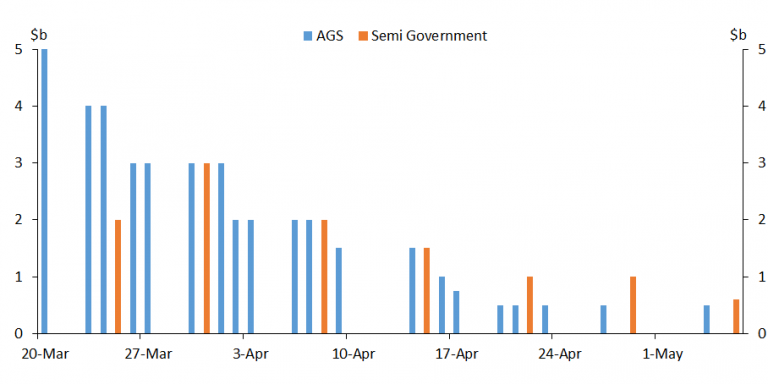

- The initial period of bond purchases by the RBA was important in clearing market congestion and facilitated a smooth and quick recovery of the market. Chart 3 shows the trend in bond purchases since the operation commenced in March.

Chart 3. RBA Government Bond Purchase Operations

Changes in AOFM issuance program

Treasury Bonds

The main focus of discussions related to the nominal bond market with investors asking:

- How large will the issuance program be, and how high could Treasury Bonds outstanding reach?

- How many new bonds lines will the AOFM issue and how large could bond lines become?

- Will the AOFM focus on a particular part of the curve? Would we maintain a long issuance strategy?

- When will the AOFM issue a new 30-year bond?

- What are the trends in investor demand and offshore holdings?

AOFM messaging

- In the absence of an official Budget forecast, the AOFM gave guidance in the form of a weekly issuance rate and plans for the establishment of new bond lines. An estimate of gross issuance for 2020-21 would need to await an official Budget update.

- High volume issuance will focus on areas of most demand and liquidity; primarily in the vicinity of the 3 and 10-year futures segments of the curve.

- Supporting the ‘long-end’ of the curve (13+ years) remains an objective in order to maintain a 30-year yield curve. A new 30-year benchmark Treasury Bond is desirable at an appropriate time, but this will depend on market conditions and assessment of demand. The AOFM is in no rush to achieve this, nor is it necessarily looking to do a large transaction when it occurs – it will be demand led and not driven by a volume objective.

- AOFM will remain highly attuned to market conditions for all issuance decisions, but the pattern of issuance and new maturity establishment it will engage in should be familiar to the market from when issuance programs were previously high (2015-2017).

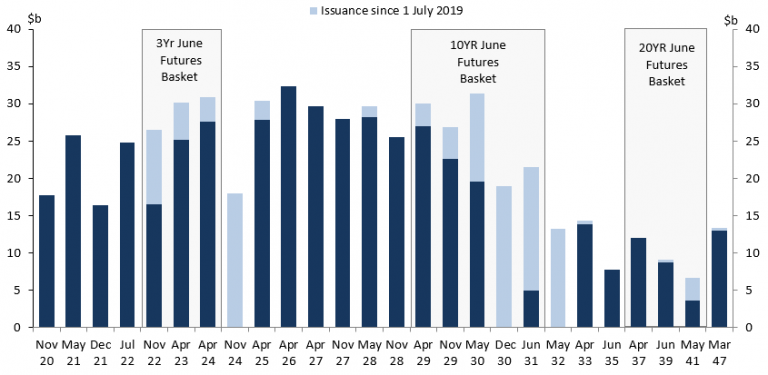

- Chart 4 highlights that issuance concentrated around the 3 and 10-year segments of the curve.

Chart 4. Treasury Bonds on issue and issuance since 1 July 2019

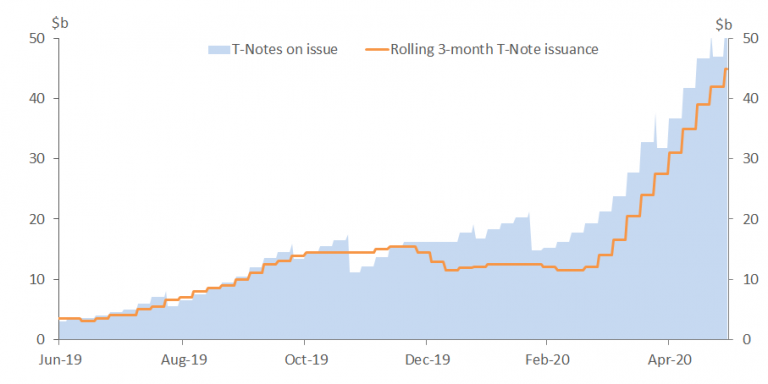

Treasury Notes

Investors were interested in the increase in Treasury Note (T-Note) issuance. There was particular interest from bank balance sheets, central banks and a good proportion of domestic fund managers. Many reported that they had bought T-Notes for the first time, or were considering them. Low secondary market liquidity was an impediment for some to invest. Investors enquired as to which intermediaries were the most active in T-Notes and whether we had seen a change in the demand profile for them, including from offshore. Investors asked:

- How large could T-Notes on issue reach? How long would levels remain elevated?

- Has AOFM formed a longer-term view on the T-Note market?

- Is there anything the AOFM can do to improve liquidity?

- Who are the leading investors in T-Notes?

AOFM messaging

- T-Notes on issue would remain elevated for at least the next year, with maturities extending out to 12 months. The amount outstanding could easily reach levels at least 5-6 times higher than had previously been planned (around $15 billion).

- The time frame on when AOFM would look to begin to term them out would depend on market conditions and the size of the funding task. As expected, T-Notes had played a vital role in managing liquidity risk for the cash portfolio during the period of market dislocation and then while the market recovered.

Chart 5. AOFM Treasury Notes Issuance

Treasury Indexed Bonds

Most interest in Treasury Indexed Bonds (TIBs) came from domestic investors who are significant holders. Initial discussions focussed on the period of market dislocation in March, which saw noticeable underperformance of the asset class and poor liquidity as seen in very wide bid/offers, or in some cases intermediaries being unwilling to make two-way prices.

As market conditions improved through May, investor discussions focused more on when we would resume issuance with confidence returning to the market. Several offshore investors noted that TIBs looked very cheap on a breakeven inflation (BEI) basis, and suggested they would be larger holders if the asset class was more liquid.

AOFM messaging

- The AOFM will maintain the TIB market according to existing policy.

- TIB issuance was paused following the period of market dislocation in March and April, however, improvements in market conditions will at some point allow the resumption of small tenders. The AOFM understands that not issuing will be helpful initially but then at some point will in itself detract from liquidity.

- While remaining conservative in the issuance of TIBs, the AOFM intends to support a functional market to the extent possible through sensible issuance decisions.

- The AOFM understands under current circumstances that it cannot look to the TIB program for meaningful contribution to the Government’s financing task.

These calls were part of an ongoing engagement program focused on maintaining a dialogue with investors.