Issue 13 | AOFM Investor Insights | August 2023 | PDF

Introduction

This edition of Investor Insights is on supporting the 30-year price point on the Treasury Bond curve. In its issuance program update on 30 June 2023, the AOFM announced plans to issue a new June 2054 Treasury Bond by syndication in the December quarter (October to December 2023). The June 2054 bond will be the third 30-year bond issued by the AOFM – the other two being the March 2047 (issued in October 2016) and the June 2051 (issued in July 2020).

The development of the ultra-long end of the Treasury Bond market, including extending the curve to 30 years was discussed in Investor Insights Issue 6. Extending the yield curve and establishing the 30-year benchmark has facilitated several objectives:

- Lengthening the portfolio’s duration, thereby reducing refinancing risk.

- Diversifying the investor base.

- Providing the AOFM with additional issuance options.

This paper discusses the following:

- Considerations on issuance volumes, lines sizes and maturity gaps.

- Sources of investor demand and recent trends.

- AOFM’s plans for supporting the 30-year benchmark bond.

Considerations on issuance volumes, line sizes and maturity gaps

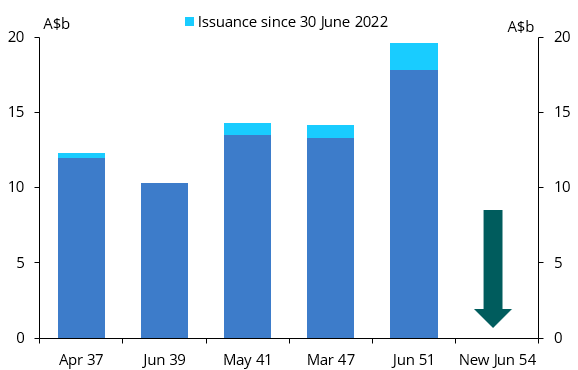

Chart 1 shows the volume on issue of the five longest-tenor Treasury Bonds and issuance by tender since July 2022. The June 2051 bond is the largest ‘ultra-long’ bond line, even though it is the most recently issued line. This mainly reflects the large size of its initial syndicated issue of $15 billion in July 2020, which came at a time of heightened funding requirements. Still, consistent investor demand has prompted the AOFM to tap the line consistently since with small, regular tenders.

Chart 1. Treasury Bonds on issue longer than 15 years.

Source: AOFM. Updated to 25 August 2023.

Peer country comparisons

Table 1 compares 30-year issuance in terms of frequency of issuance, gaps between maturities, and volumes on issue. Australia has only had a 30-year benchmark for a relatively short time. Australia has one bond line over 25 years, a relatively wide gap between the two longest lines and the lowest proportion of ultra-long bonds outstanding.

Table 1. Peer countries’ 30-year bond issuance.

Country |

No. of 30-year bonds issued since 2010 |

No. of 30-year bonds on issue |

Avg. line size (USD billion) |

Avg. gap between 30-year lines (years) |

30-year proportion of total bonds outstanding (%) |

|---|---|---|---|---|---|

| United States | 55 | 20 | 71 | 0.25 | 8.0 |

| Japan | 48 | 29 | 17 | 0.40 | 7.2 |

| UK | 10 | 10 | 32 | 0.94 | 14.1 |

| Italy | 9 | 5 | 14 | 1.02 | 3.5 |

| Germany | 7 | 3 | 25 | 1.67 | 6.5 |

| France | 6 | 5 | 29 | 1.23 | 6.8 |

| Canada | 5 | 4 | 19 | 2.33 | 11.5 |

| Australia | 2 | 1 | 13 | 4.25 | 2.4 |

Source: Refinitiv, AOFM. 30-year bonds are defined as 25 to 35 years. Updated to 25 August 2023.

The 30-year bond is the focal point for investor demand beyond the traditional 10-year benchmark area both in AGS and other sovereign bond markets. Consistent investor feedback is that four-year gaps between new 30-year AGB benchmark lines is a little long. While many are relatively indifferent between two- or three-year gaps, all highlight the importance of liquidity. There is a balance to be achieved between having more smaller, potentially less liquid benchmark lines and fewer larger lines.

The new June 2054 bond will have a three-year gap to the current 30-year benchmark and will be around six to nine months longer than 30 years at the point of issue. Experience from previous 30-year syndications shows that most ultra-long bond investors have the flexibility to buy longer than 30 years – for a small minority that do not, the period when the new bond becomes shorter than 30 years can be an additional source of demand and liquidity.

Sources of investor demand and recent trends

Syndicated issuance

The AOFM endeavours to calibrate issuance of ultra-long bonds to end investor demand. The investor base for 30-year bonds is quite different from shorter-dated bonds, demonstrated by investor allocations in previous syndicated deals and trends in secondary market turnover data by bond line. Demand for long-dated Australian dollar bonds has grown steadily as the AOFM has developed the market. Offshore private sector investors provide the primary source of demand, with domestic investors and offshore reserve managers tending to heavily weight their bond holdings towards 0-12 year maturities.

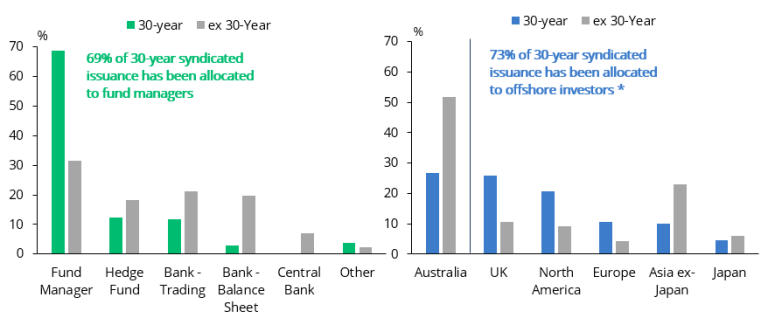

Chart 2 shows that 30-year syndications have attracted a much higher amount of fund manager participation, including asset managers, insurers and pension funds. Around 69% has been allocated to this broad category compared to 32% for other syndicated deals. Over 70% of 30-year allocations have been to offshore investors, with the UK (26%) and North America (21%) as the most prominent regions.

Chart 2. A comparison of syndication allocations by type and geography.

Source: AOFM. *The geography component excludes trading accounts, which are mainly domestic based.

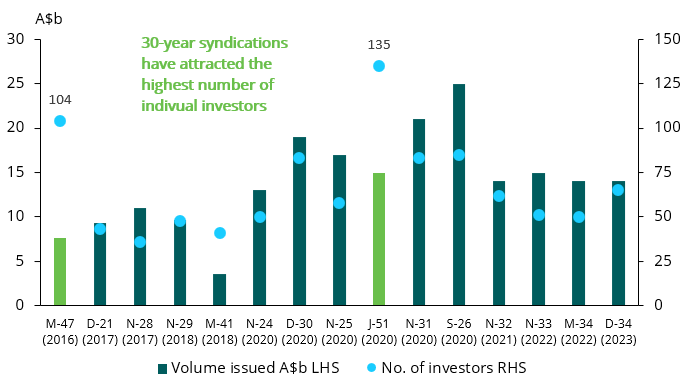

Even though fewer investors overall buy 30-year bonds compared to shorter-dated bonds, Chart 3 demonstrates that 30-year issuance has attracted the largest number of individual investors in syndications. This demonstrates that syndications are significant supply events for 30-year bonds.

Chart 3. Volume issued in syndications since 2016 and the number of individual investors.

Source: AOFM. Excludes tap syndications.

Secondary market turnover

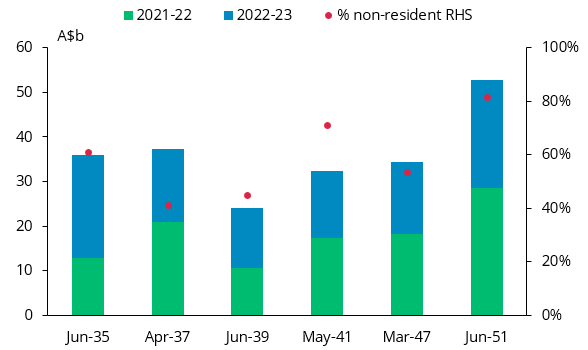

The AOFM has been collating secondary market turnover in individual bond lines from intermediaries since July 2021. Ultra-long bonds generally exhibit lower turnover than shorter-dated bonds, especially those comprising the more liquid three- and ten-year futures contracts. That said, as chart 4 demonstrates, the June 2051 bond has the highest turnover of any bond longer than the 10-year contract – this reflects its status as the ‘benchmark’ 30-year bond, which is especially relevant for offshore investors.

Chart 4. Secondary market turnover in long bonds and non-resident proportion.

Source: AOFM. Excludes trading accounts.

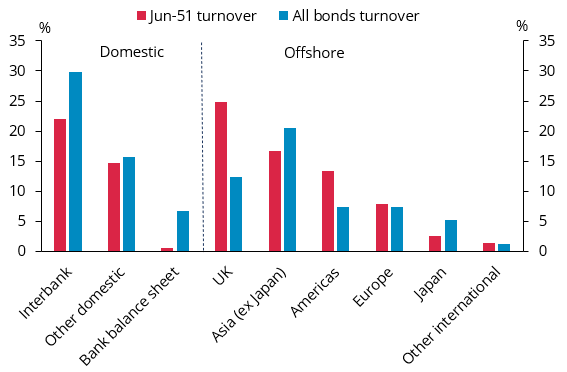

Chart 5 shows that the UK exhibits the highest proportional turnover in the 30-year bond, with around 25% of total turnover in that line (including interbank). Asia ex-Japan and the Americas are also active regions in the 30-year bond. Domestic non-bank investors have comprised around 15% of turnover in the June 2051 bond over the last two years, slightly less than their overall turnover proportion.

Chart 5. Proportion of turnover by region – June 2051 v All bonds.

Source: AOFM. Excludes turnover with the RBA.

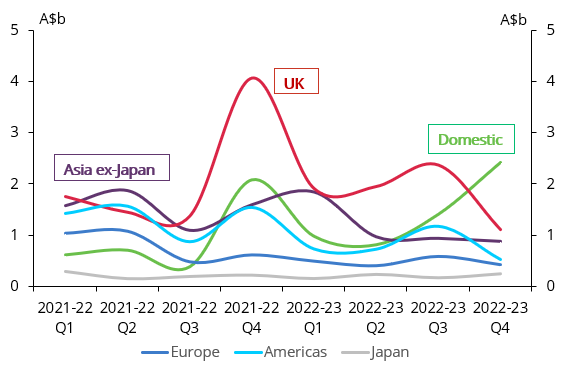

More frequent quarterly data shows how turnover in the June 2051 bond has varied by region over the last two years. Bank feedback suggests that domestic relative value investors will also buy other ultra-long bonds if they perceive them to represent value. In contrast, offshore investors are more focused on the 30-year benchmark.

Chart 6. Quarterly turnover in the June 2051 bond by region.

Source: AOFM

Drivers of Investor demand

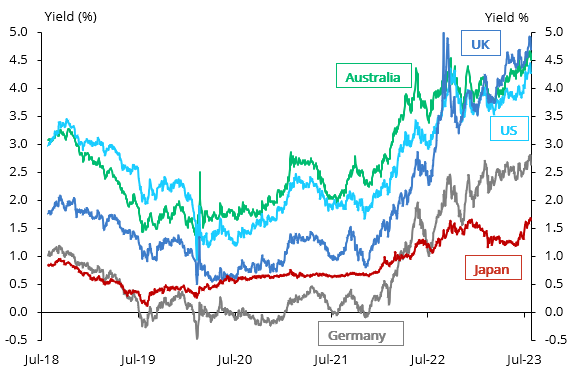

Various factors influence investors' allocations to AGBs. These include outright yield levels, spreads to other sovereign bonds, future yield expectations, the relative steepness of the AGB curve, views on the currency levels and hedging costs, and the diversification benefits of holding AGS in a portfolio of multiple sovereigns.

Chart 7. A comparison of 30-year sovereign bond yields.

Source: Refinitiv. Yields updated to 24 August 2023.

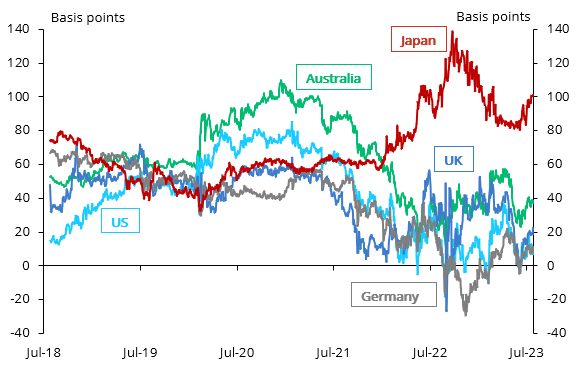

The relative slope of the yield curve provides an important measure of the relative value of ultra-long bonds for investors but is also a strong signal to the AOFM that the 30-year segment of the curve is fully established. Chart 8 demonstrates that while the 10s/30s spread remains steeper than other sovereigns (excluding Japan), it has flattened considerably since 2021. There is now a strong relationship whereby the ultra-long part of the yield curve flattens as yields rise and steepens as yields fall. This behaviour is consistent with other established ultra-long bond markets.

Chart 8. Slope of sovereign bond curves | 10s/30s

Source: Refinitiv. Yields updated to 24 August 2023.

AOFM’s plans for supporting the 30-year benchmark bond

Issuance size

The June 2054 syndication will be a ‘benchmark’ size. However, it will be smaller than the $15 billion syndicated deal of the June 2051 bond undertaken in July 2020, given the now considerably smaller 2023-24 financing task.

Some scaling of the bids can be expected if demand exceeds supply at the issue yield. The AOFM will, as it normally does, seek to allocate the majority of the deal to ‘real money’ investors. However, a modest amount will be allocated to trading accounts, including hedge funds, to assist secondary market trading in the new bond.

Issuance post-launch

Further issuance into the new bond line will be by small tenders. The size and timing of tenders will be informed by demand from price makers and investor feedback. The AOFM can still issue into any other ultra-long bond line by tender in response to market demand.