Issue 12 | AOFM Investor Insights | April 2023 | PDF

Introduction

This edition of Investor Insights considers trends in Australian Government Securities (AGS) demand from the Australian superannuation sector. AGS appeals to a wide range of investors. For domestic investors, including the superannuation sector, AGS are the credit risk-free benchmark to which all other asset classes are compared.

Domestic investors include bank balance sheets, fund managers, superannuation and pension funds, insurance funds, and public sector investors. Over the last few years, the AOFM has increased its engagement with superannuation funds, partly due to the ongoing growth of funds managed by the sector and by industry consolidation resulting in fewer but much larger funds.

This paper discusses the following:

- Trends in the domestic investor base for AGS and the superannuation sector's holdings of AGS.

- The size and growth of Australia’s pension (superannuation) system which should support ongoing and increasing demand for AGS.

- The key drivers of superannuation asset allocation between asset classes and within fixed income, including for AGS.

Trends in domestic holdings of Australian Government Bonds

Chart 1 shows that non-bank domestic investor holdings of Australian Government Bonds (AGBs)[1] have generally trended upward since 2010 and were approaching around 20% of the AGB market until the pandemic-induced financial shock in 2020. Since 2020 domestic holdings have fallen only slightly in outright terms, although they have declined to around 11.5% in proportion terms.

Chart 1. Domestic investor holdings of AGBs and proportion held

Source: Australian Bureau of Statistics (ABS)

Composition of the domestic investor base

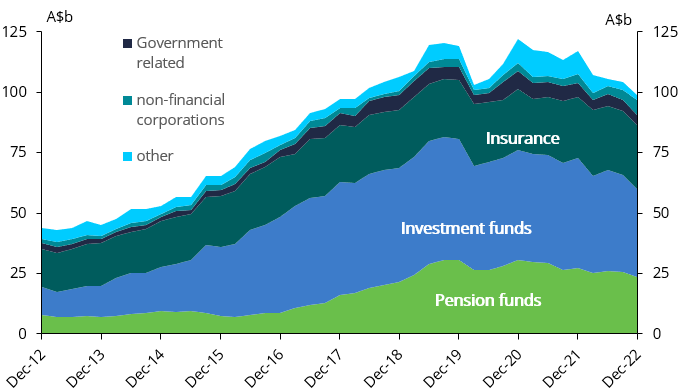

Chart 2 shows the main categories of domestic (non-bank) holdings as reported by the ABS – the most prominent segments being pension funds (superannuation), investment funds and insurers. Pension funds comprise around A$23.5 billion as of December 2022 which is down from the highest reported amount of A$30.8 billion in September 2019. It’s likely that overall superannuation AGB holdings are a little higher than that reported by the ABS, since many funds (including self-managed super funds) hold AGBs via exchange-traded funds which would be included in the ‘Investment funds’ category.

Chart 2. Domestic non-bank AGB holders by category

Source: ABS

Growth of the superannuation sector

As of December 2022, the total funds under management of the Australian superannuation sector was $3.4 trillion[2] making it the 4th largest pension market globally[3]. Continued growth is supported by legislation that requires employers to pay at least 10.5 per cent of employees’ earnings into superannuation – this will increase to at least 12% by July 2025. The Australian Treasury projects that total superannuation assets under management will reach almost 250% of GDP by 2060.[4]

Chart 3. The total value of superannuation assets under management

Source: Australian Treasury – 2021 Intergenerational Report

Drivers of superannuation asset allocation

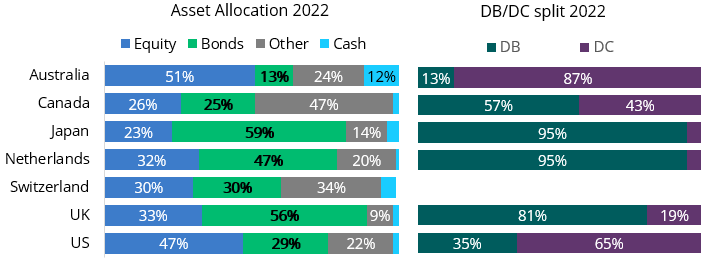

Chart 4 shows that Australia’s total allocation to fixed income in the pension sector is relatively low by global standards. Australian superannuation is a defined contribution (DC) system rather than a defined benefit (DB) – as a result, the allocation to growth assets such as equities is much higher than global peers.

Chart 4. Global pension industry allocation to fixed income

Source: Willis Towers Watson

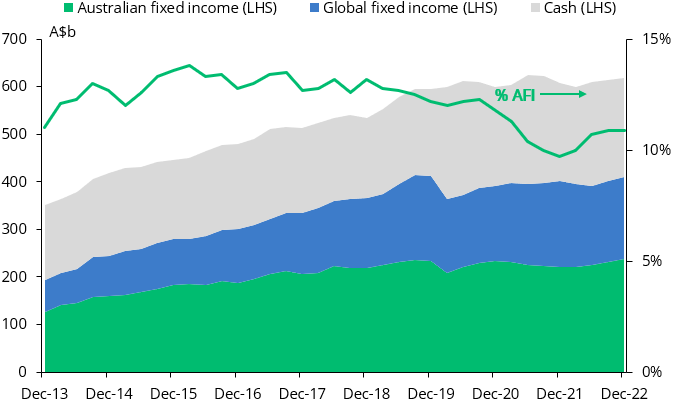

Chart 5 demonstrates, Australia’s relatively small fixed-income allocation is still significant in outright terms. As of December 2022, the allocation to Australian fixed income (AFI) by funds with more than six members was at a record high of $237 billion.

Chart 5. Superannuation industry allocation to fixed income (excluding SMSFs)

Source: Australian Prudential Regulation Authority (APRA)

Notably, the Australian pension system has a relatively high proportion of cash compared to the rest of the world. The main reason is that as Australia is a DC system, members may elect to hold cash as a defensive asset class. Also, funds themselves value liquidity since members can switch funds and investment options, and funds may need to meet redemptions, unlike in DB systems where members do not choose asset allocations. Lastly funds may require cash to meet margin calls on hedges (held to reduce foreign currency risks).

Demographics and an ageing population

Like most of the developed world, Australia’s population is ageing. This is leading to a gradual shift toward more defensive asset allocations, including fixed income. Individuals who do not choose their asset allocation are placed into default funds called ‘MySuper’. Around 30% of all superannuation is in MySuper accounts which typically have a balanced asset allocation. Many super funds offer a ‘lifecycle’ default allocation, which automatically adjusts the asset allocation as members age - from growth assets for young members to more defensive allocations as they approach retirement. Offsetting this impact is that in the retirement phase, these defensive assets may be sold to generate an income stream. As Chart 3 demonstrates, however, the overall growth from higher contributions will significantly outpace drawdowns in the retirement phase for the foreseeable future.

Performance benchmarks

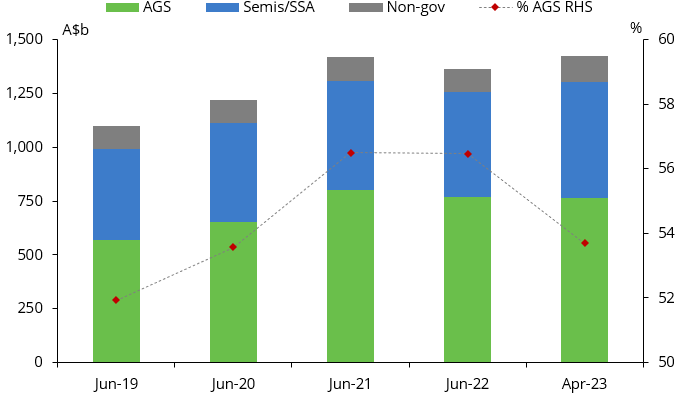

The most widely followed performance benchmark for AFI allocations is the Bloomberg AusBond Composite 0+ Yr Index. Under the ‘Your Future, Your Super’ legislation, superannuation funds must report their AFI performance against this benchmark. Chart 6 shows that the proportion of AGS in the index rose to over 56% in June-22, although it has fallen slightly in 2022-23. The 2022-23 Budget forecast that AGS outstanding would continue to increase from $895 billion in June 2022 to $1.16 trillion in June 2026, meaning that AGS should remain well above 50% of the index even with increased semi-government issuance.

Chart 6. Growth of the Ausbond composite 0+ Yr index

Source: Bloomberg

On average, superannuation funds tend to be 'overweight' semi-government and corporate bonds compared to AGS. Funds can also use futures to manage duration exposure rather than the underlying bonds. That said, AGS's greater liquidity and stronger credit compared to other domestic fixed-income securities are an attraction for holding AGS. Another factor is that the annual performance test for MySuper funds provides a disincentive for funds to deviate too far from the index weightings.

A topic of interest to Treasury Indexed Bond (TIB) investors and price makers is that the current MySuper performance benchmark excludes TIBs, discouraging holding TIBs in these portfolios. Following a public consultation of the ‘Your Future, Your Super’ laws, the Government has proposed new benchmarks for fixed income allocations for MySuper products. The 'composite' index is proposed to be the Bloomberg Ausbond Master 0+ Yr Index, which has around a 3 per cent weighting by market value to TIBs. It will also include specific benchmarks for credit and government bonds (excluding TIBs). This would result in modest allocations towards TIBs by super funds, which in a relatively small TIB market, could be impactful for overall investor demand for TIBs.

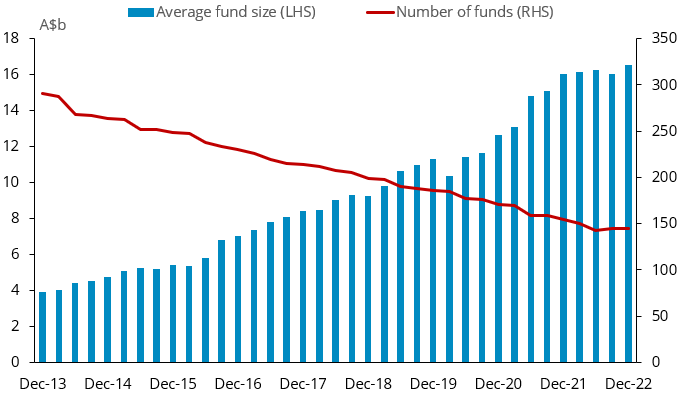

Industry consolidation

Another factor potentially affecting AFI allocations is the trend toward consolidation and mergers of superannuation funds creating fewer but much larger funds. Chart 7 shows that over the last ten years, the number of individual funds with more than $50 million AUM has halved, while the average fund size has increased more than four times. As of June 2022, the combined assets of the ten largest super funds exceeded A$1.5 trillion.[5]

Chart 7. Superannuation industry consolidation

Source: APRA, entities larger than $50 million

Allocations to fixed income and AGS vary between funds, which reflect, among other things, the composition of the member base and different risk and return objectives. Many of the largest funds increasingly manage their AFI portfolios in-house rather than outsource to external managers to reduce fees.

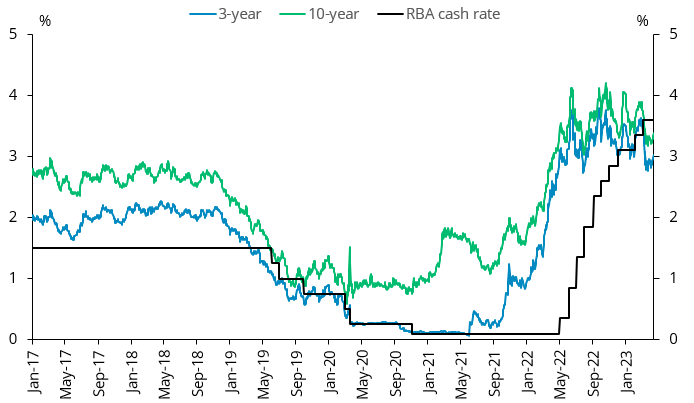

Impact of a rising interest rate environment

The most significant impact on financial markets since 2022 has been rapid central bank monetary policy tightening in response to rising inflation. As Chart 8 shows, this has led to yields rising across the Treasury Bond curve from the record-low yields experienced in 2020 and 2021. Higher yields are attractive for investors, although by no means the only factor in asset allocation. Some investors had commented that higher yields enhance the diversification benefits of adding fixed income to a portfolio compared to when yields were extremely low in 2020 and 2021. Several superfunds have indicated that they have or intend to increase their allocation to fixed income because of an expected global growth slowdown and concerns over the liquidity risk of some growth assets in a more volatile market.

Chart 8. Treasury Bond yields

Source: Refinitiv

Summary

The domestic superannuation sector is an important source of demand for AGS. Structurally the Australian pension system will continue to have a lower allocation to defensive assets, including government bonds, than defined benefit systems; however, even a small proportional shift toward fixed income and AGS will be significant in absolute terms. The key drivers underpinning the long-term growth of demand for AGS include the ongoing increase in retirement savings from population growth and higher compulsory savings rates; changing risk and return preferences with an aging population; industry consolidation and mergers; and changes to performance benchmarks which include a high proportion of AGS.