Australian Business Economists luncheon | Sydney

Anna Hughes, CEO

“50 Shades Greener: the AOFM’s move into labelled bond issuance and the impact on the depth and breadth of the investor base."

Before I offer my reflections, I would like to acknowledge the Traditional Custodians of the land on which we gather today, the Gadigal people and pay my respects to their Elders past, present, and emerging. We are on land that has been cared for by the Gadigal people for thousands of years. Their deep spiritual connection to this land is something that has shaped its landscapes, culture, and history in ways that we benefit from today. It is a privilege to stand on this ground and share in its beauty and resources, a privilege made possible by the resilience and enduring presence of its First Peoples.

I would like to thank the ABE for the invitation to speak today. I see today as an opportunity to share the AOFM’s perspective on the issuance of Australia’s inaugural Green Treasury Bond, the lessons we learned and the future of labelled issuance. I will also provide my perspectives on the AOFM’s upcoming funding task, and how we will navigate through market uncertainty. Given the market’s ongoing turbulence and a softening economy, our thinking on a few issues may well change. As always, when our thinking does change, we will communicate it clearly to the market. I would also ask that you be mindful that I can only speak on matters directly relevant to the AOFM.

With my verbal disclaimer out of the way, I would like to turn to Australia’s inaugural Green Treasury Bond and the lessons we learned through the process.

Australia’s inaugural Green Treasury Bond, lessons learned and the future of labelled issuance

It is the third of June 2024. The alarm goes off a little bit earlier than usual for the AOFM team as we plan to meet in the office in time for the JLM go/no-go call. While there is usually a bit of an office buzz on syndication days, today’s buzz feels more monumental. After more than 12 months of dedicated work, we have finally made it to the launch day of Australia’s inaugural Green Treasury Bond. At the beginning of the process, we set ourselves several goals with one of them being to attract investors that have not participated in previous AOFM syndicated issues. Would today be the day we make Australia’s investor base ’50 shades greener’?

And what about the government’s policy objective of boosting the scale and credibility of Australia’s green finance market? There was also the question of a ‘greenium.’ While not a crucial KPI we were hopeful that the yield of the first green bond would be lower than our estimate of the fair value yield on the Treasury Bond yield curve.

So how did we go?

50 shades greener?

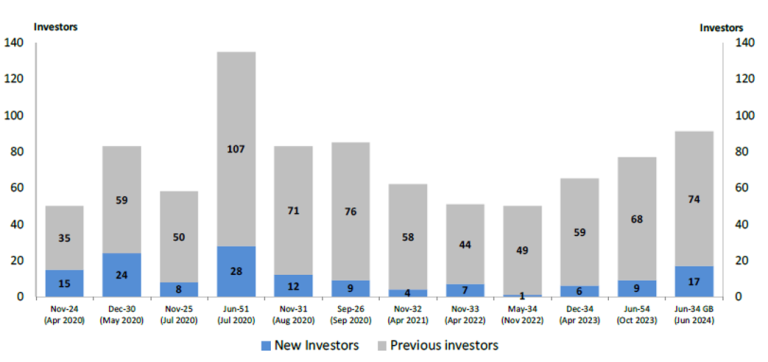

As we all know, a diverse global investor base increases the resilience of the bond market and safeguards the government’s access to finance in a crisis. It is why an objective of the green bond program was to contribute to further diversification of the AGS investor base. The chart shown on this slide reflects the new investors in the green bond deal and compares it with the deals in the past few years. Out of the 91 individual investors in the deal (excluding bank trading accounts), 17 investors were new to syndications. Several of these investors had bought AGBs in the past but only in the secondary market and never via primary. However, given the difficulties some investors face participating at primary, we were pleased the green bond allowed them to be involved in this syndication.

Chart 1: New investors in syndicated deals

Source: AOFM. Investor numbers excludes trading banks. Different geographical regions of the same parent investor are counted separately.

Notably, only syndications of 30-year bonds have attracted more investors.

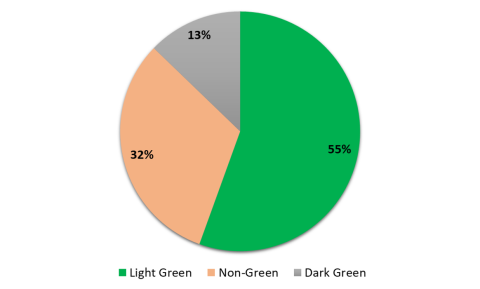

A further measure of success was the type of green investor that was attracted to the deal. While not a definitive guide of any sort, the AOFM has attempted to categorise the investors who participated in the deal into Dark Green, Light Green, and Non-Green categories. The categorisation is based on investor feedback during the roadshow meetings, guidance from a JLM bank on the type of investors, how the investors integrate ESG into their portfolios, and if the investors are a signatory to the United Nations’ Principles for Responsible Investment (UN PRI).

As you can see from this chart, Dark Green investors, who are mostly located offshore, only received a small allocation. We will come to why in a minute.

Chart 2: Green Bond investor Categories (by allocation amount)

Source: AOFM. Analysis is based on investor feedback during the roadshow meetings, how the investors integrate ESG into their portfolios, and if the investors are a signatory to the UN PRI.

Meanwhile, 55% of the deal was allocated to Light Green investors who apply ESG screening to their portfolio or integrate ESG into their portfolios in some way. This reflects a growing trend among investors to align their investments with environmental impact. The deal also saw strong demand from domestic investors in the Light Green category, indicating significant local interest in supporting Australia’s Green Bond program.

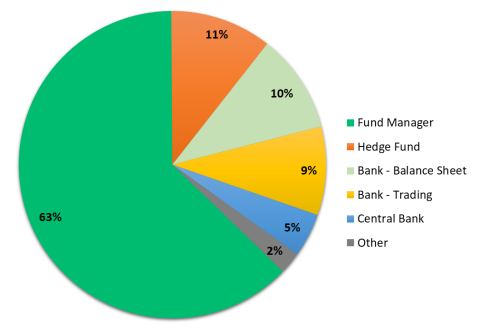

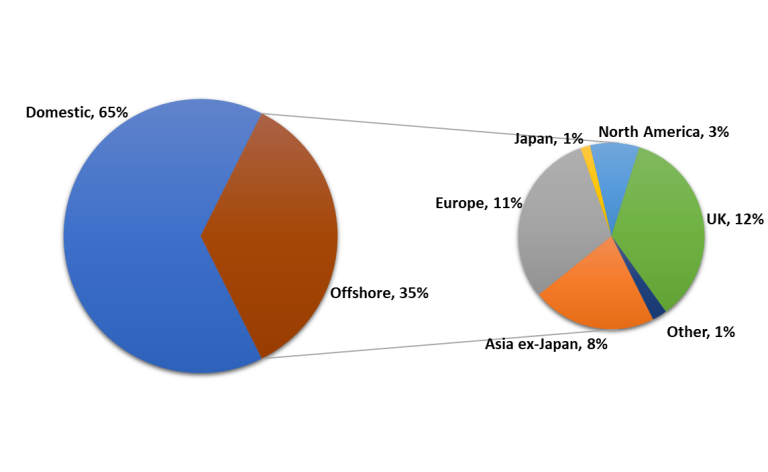

Greenness aside, the deal saw a much higher allocation to fund managers (63%) compared to what we would normally see for a vanilla Treasury Bond with similar maturity. In fact, fund manager participation was more akin to what we see in ultra-long bond trades. Allocations to balance sheets (10%) and central banks (5%) were slightly lower than similar tenor bonds. The overall allocation to ‘real money’ of 80% was the highest of any previous deal, reflecting the smaller size of the deal and strong underlying demand. In fact, the proportion could have been even higher with scaling applied across all investor types. Investors are increasingly focussed on ESG and the AOFM is of the view that the labelling of the bond contributed to strong ‘real money’ support for the deal. A further positive for the deal was the staunch support shown by domestic investors who made up 65% of the final allocations.

Chart 3: Green Bond investor by type

Source: AOFM

Chart 4: Green Bond investor by geography

Source: AOFM

Given the incredible amount of effort that went into our first ever deal roadshow, the AOFM was keen to understand our conversion rate. We were extremely pleased to observe a strong turnout at the syndication. Out of the 91 unique investors (105 including bank trading accounts) who participated in the deal, the AOFM had met 61 investors as part of the roadshow. This represents a rate of 67%, which is a significant indicator of investor engagement and support. 46% of the investors who were allocated bonds in the deal had met with the AOFM in-person during the roadshow.

The success of the European leg of the roadshow is demonstrated by the largest proportion of European accounts participating in a deal of this tenor (outside of a 30-year bond syndication).

The robust participation of investors in the roadshow and syndicated deal demonstrates investor confidence in the green bond program and their commitment to supporting it. In our mind, this sets a positive precedent for future green bond issuance.

So, what about pricing? And did we meet the Government’s policy objectives?

Greenium

As I mentioned earlier, achieving a greenium was not an explicit KPI although pricing and achieving value for the taxpayer is obviously important. Given the amount of administrative effort it takes to issue labelled bonds, a greenium is welcome. That said, the success of the deal and the willingness of investors to pay a premium would suggest that the policy objectives of boosting the scale and credibility of Australia’s sustainable finance market were important to investors, particularly domestically.

So how did the deal play out?

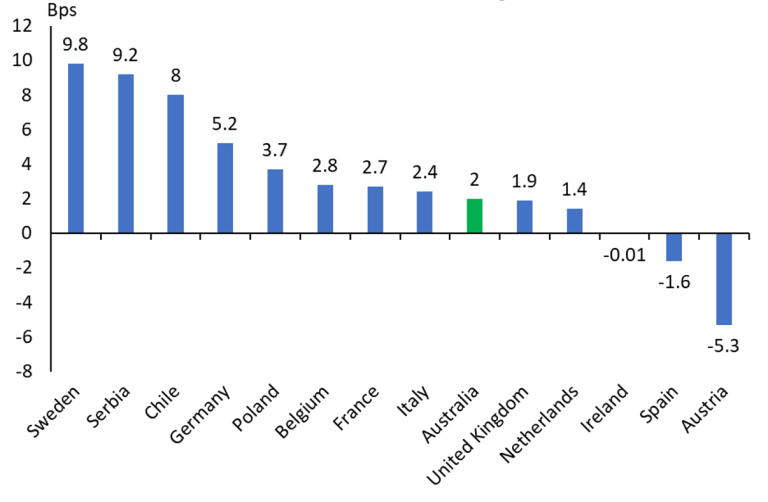

Initial price guidance for the issue was set at a spread of -5 to -1 basis points to the implied bid yield for the primary ten-year Treasury Bond futures contract. There was a quick start to the bookbuild on Monday, 3 June, after the launch. The book reached $20 billion after midday Monday and $25 billion by Monday afternoon. This allowed the AOFM to reframe the pricing to EFP –5 to –3 basis points. The bond was priced on 4 June 2024 at an EFP of -3 basis points, the middle of the launch range. By our estimates, this implied a greenium of around 2 basis points.

Chart 5: Greenium across sovereigns

Source: IMF - How Large is the Sovereign Greenium? April 2023; AOFM.

The market of course sets the clearing price of green bonds and there has clearly been some erosion in greenium in the period since issue. We will monitor this over time and it may be that greeniums follow trends in overseas markets.

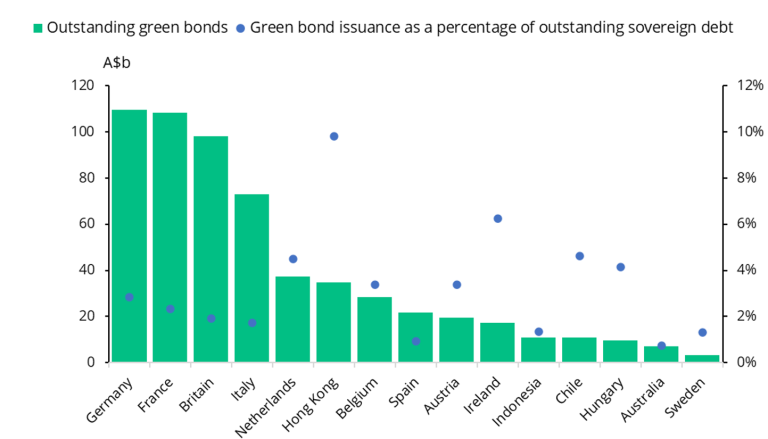

Chart 6: Green bonds on issue across sovereigns

Source: Bloomberg, as at 28 June 2024

It will be interesting to see how this develops, particularly as we introduce a program of tenders to build the size of the line over time.

Insights gained

So, what other insights did the AOFM gain through the process?

One key take-away is the importance of consultation and engagement. We undertook an extensive round of investor consultations when we were drafting our Green Bond Framework. By listening to investors, we were able to ensure that our Framework is “best in class” reflecting investor views on issues like exclusion categories, limits on refinancing existing expenditure, and reporting arrangements. Many investors felt like they had been part of our green bond journey, and from our perspective they made important contributions.

A strong positive learnt from the deal was the great support from our domestic investor base. We understood that for some paying a greenium would be quite difficult and we appreciated that many of them still participated. We feel their dedicated support for and understanding of the Green Bond Framework allowed this.

Despite the positive feedback and high engagement from investors about the green bond issuance prior to and during the roadshow, some investor groups were noticeably absent from the deal. This included a substantial portion of European investors (noting that we still had the largest proportion of European accounts participating in a deal of this tenor), and some of the larger North American investors. At this stage, the major considerations were price; investors failing to get approval or having limits placed on them due to some concerns around Australia’s climate policies and ongoing issues with coal exports. Some investors also flagged the difficulties they have with buying at syndication.

In short, we were disappointed with the offshore support particularly since we had been engaging regularly with a number of these investors either directly or via the UN PRI Collaborative Sovereign Engagement on Climate Change process and then via the roadshow. Many dark green investors did not participate despite providing positive feedback and several saying they wished to support the deal. For some, the sustainable finance team approved investing in our green bond, but the portfolio manager balked at the price. The lesson for us is that we still have work to do with some investors around building support for Australia’s green bond program.

The way forward for Green Treasury Bonds and the future of labelled issuance

The plan is for Green Treasury Bonds to form a regular program of issuance. After each Budget update, the Green Bond Committee will assess new Eligible Green Expenditures and decide which projects are eligible for financing using the proceeds of Green Treasury Bond issuance.

From here, the AOFM will focus on the liquidity of the June 2034 line by issuing regularly into this line. The AOFM announced on 28 June 2024 that issuance via tender of Green Treasury Bonds in 2024-25 is expected to be around $2 billion. This is significantly less than the amount of Eligible Green Expenditures able to be financed by Green Treasury Bonds. The AOFM is retaining issuance capacity for syndicated launches of new lines so it can develop a ‘curve’ over time.

As for reporting, Australia will provide annual transparent reporting on the allocation of proceeds towards the Eligible Green Expenditures (allocation reporting), as well as the positive environmental impact and social co-benefits, where available, of those expenditures (impact reporting). This will be published on the AOFM website.

Reporting will be at an aggregated portfolio level rather than against each individual bond line. Ongoing annual allocation and impact reporting will commence in 2025.

As for other types of labelled issuance, this will be a decision for the Australian Government.

AOFM’s upcoming issuance task and how the organisation will navigate through ongoing market turbulence

I would like to turn now to the AOFM’s upcoming issuance task.

Let me start with the Australian Government’s budgetary position, and how it will impact our issuance task over the year ahead.

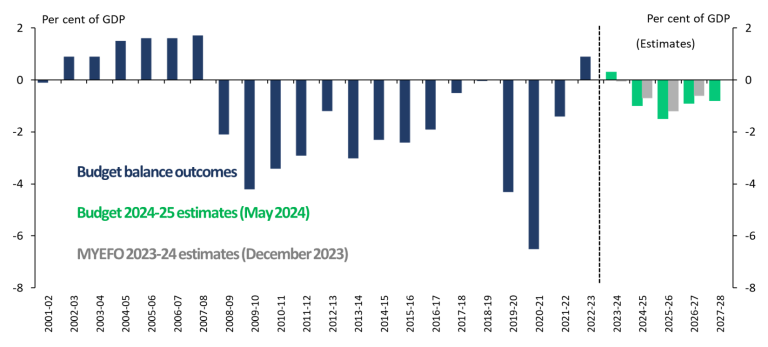

Chart 7: Australia's budget balance

Source: Treasury – Budget 2024-25.

As you would have seen from the latest Commonwealth Budget, an underlying cash surplus of $9.3 billion is forecast for fiscal year 2024, an improvement of $10.5 billion compared to a deficit of $1.1 billion forecast in the 2023-24 MYEFO. With the government’s budgetary position strengthening we had already revised down our issuance task from $75 billion to $50 billion at MYEFO.

With the end of the fiscal year having just passed I can confirm that our 2023-24 Treasury Bond issuance was $50 billion (including our green bond) while we issued $3.55 billion of Treasury Indexed Bonds. Our cash position remains strong.

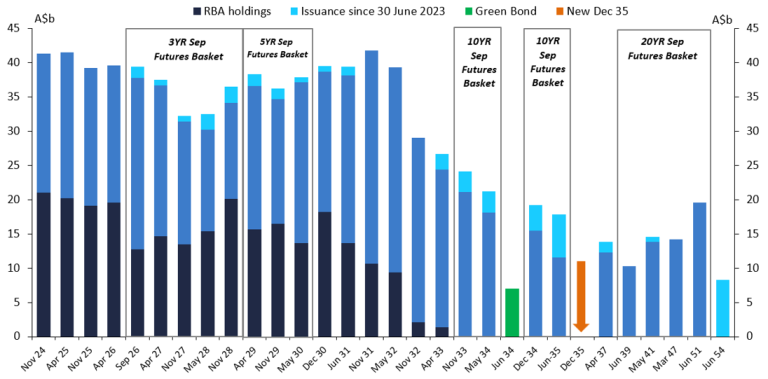

Turning to this year, the government is forecasting a deficit of $28.3 billion in 2024-25. In addition to funding the deficit, we have two bond maturities during this fiscal year, the November 24 and April 25 which will total a little over $80 billion. This represents the highest refinancing task we have ever faced. We plan to meet our target primarily by issuing around $90 billion of Treasury Bonds and drawing down cash reserves.

Chart 8: Treasury Bonds on issue

Source: AOFM. As at 28 June 2024.

As noted earlier, around $2 billion of Treasury Bond issuance in 2024-25 will consist of Green Treasury Bond tenders.

The wider range for Treasury Indexed Bonds indicates that the flexibility to respond to investor demand and market conditions is there.

We will continue to maintain at least $25 billion in Treasury Notes on issue while conducting a tender most weeks.

The projected composition of financing for this fiscal year is consistent with a key element of our 2023-24 strategy to smooth the increase in AGS issuance across fiscal years. As I noted last year, funding only the minimum required amount would have led to a large proportional increase in annual issuance this year. In our view, smoothing the bond issuance profile is helpful for market functionality. Feedback suggests that investors and intermediaries remain comfortable with AOFM’s approach.

Let me turn to the question of new benchmark Treasury Bond lines. As you would have seen last Friday, the AOFM plans to issue a new December 2035 Treasury Bond in the September quarter (by syndication and subject to market conditions). A new 2036 line will be considered next calendar year. No new ultra-long lines will be established this fiscal year. Our broad approach will be to consider a new 30-year benchmark only when the existing 2054 rolls down to around 28 years to maturity. We will, however, look to conduct small regular tenders into this sector.

Our support for the inflation linked bond market will continue. We have announced a flexible range of $2 billion to $5 billion in issuance and the market should expect issuance to be well calibrated to meet investor demand. One issue we are giving some thought to is how to respond to the move from quarterly to monthly CPI which we expect will become a reality from late next year. An option we will consider is to issue linkers based on the more common international formulae with inflation indexation interpolated monthly rather than as an average of the last 2 quarters. We have plenty of time to ponder this which is helpful given that there will inevitably be a lot of consultation, planning and design work required with any changes. We will have more to say on this in due course.

In summary, the launch of the Green Treasury Bond is a significant green milestone and demonstrates Australia’s strong commitment to achieving net zero and other emission reduction targets and to improving environmental outcomes. We were extremely pleased with the success of the deal and will now work hard to ensure that reporting is in line with international best practice. We will also work hard on bringing more of the dark green investors into Australia’s green bond market.

As for the year ahead for issuance, deteriorating Budget forecasts and a significant refinancing task looks like they will be set against the uncertain backdrop of market conditions. For the AOFM as an organisation, we will need to stay focused on the fundamentals of transparency and predictability. Our relationship with the markets is important regardless of any uncertainty and we will continue to work hard to protect those relationships.

Thank you.