Issue 19 | AOFM Investor Insights | May 2026

Introduction

This edition of Investor Insights examines recent trends in the Australian Government Securities (AGS) investor base. We last profiled the investor base in Investor Insights Issue 3 in 2020, and since then there have been several key developments. The volume of AGS on issue has increased substantially, and the Reserve Bank of Australia (RBA) has become a significant holder through its quantitative easing program. Despite these changes, the overall structure of the investor base has remained broadly consistent, with shifts in the composition and relative shares of key investor groups.

This paper discusses:

- recent trends in offshore investor demand

- the drivers of offshore demand amid heightened market volatility

- trends in the domestic investor base

- insights from secondary market turnover data

Growth in the government bond market

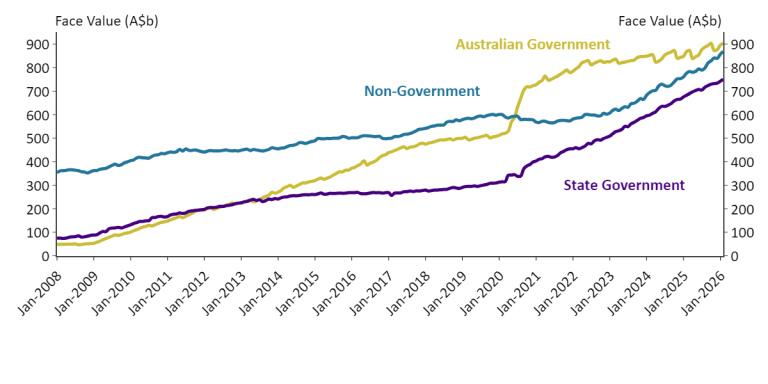

A clear development has been the sustained growth in the supply of government and high-grade non‑government AUD-denominated bonds, with issuance volumes remaining elevated since the COVID‑19 pandemic. This expansion in AUD fixed income supply has contributed to a deeper and more dynamic domestic bond market.

Chart 1. Growth in Bonds on issue in Australia

Source: RBA, AOFM.

Recent growth in offshore investors

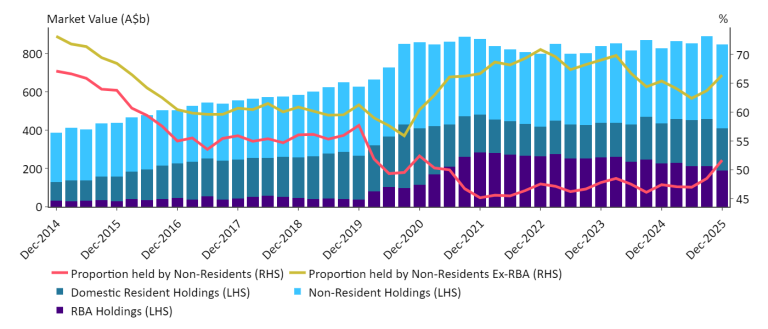

The share of Australian Government Bonds (AGBs) held by non‑resident investors has risen steadily since mid‑2025, reaching around 52 per cent in December 2025—the highest level since September 2021.

Chart 2 illustrates AGB holdings by investor type. Non‑resident holdings are shown in light blue, RBA holdings in purple, and domestic investor holdings in green. The red line shows the non‑resident share of total bonds outstanding, while the gold line shows the non‑resident share excluding RBA holdings (the free float).

As of December 2025, non‑residents held around two‑thirds of the free float. This gap between the headline and free‑float measures is expected to narrow as bonds held by the RBA mature.

Chart 2. Non-Resident holdings of Australian Government Bonds

Source: Australian Bureau of Statistics (ABS), RBA, AOFM. AGBs are Treasury Bonds and Treasury Indexed Bonds.

The offshore AGS investor base is large and diverse, encompassing FX reserve managers, asset managers, insurers, offshore banks and hedge funds across a wide range of regions.

Continued growth in FX reserve holdings

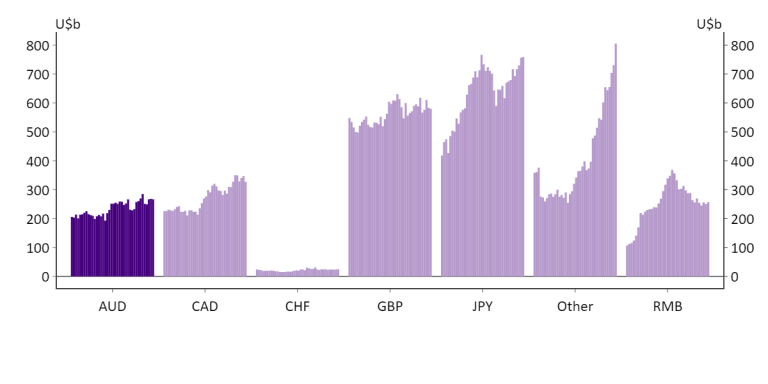

FX reserve managers represent the largest offshore investor group, potentially holding around half of non‑resident AGB holdings—equivalent to roughly one‑quarter of the total AGB market.

As shown in Chart 3, Australian dollar holdings by FX reserve managers have increased gradually and currently total around US$266 billion, or just over 2 per cent of global FX reserves. More than 80 per cent of the top 30 reserve managers report holding AGS.

AGS remain a core component of central bank AUD allocations due to their liquidity and capital preservation characteristics. In recent years, some reserve managers have also increased allocations to semi‑government securities as that market has expanded. While many reserve managers favour shorter maturities, others trade more actively across the yield curve.

Chart 3. Central bank FX reserve allocations excluding USD and EUR, 2016–2025

Source: IMF.

Drivers of offshore demand

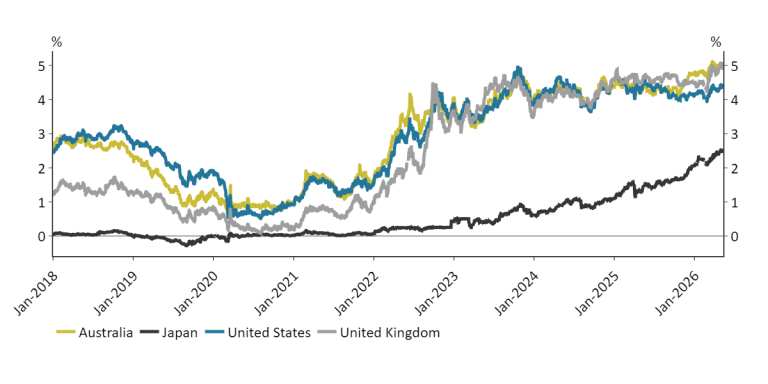

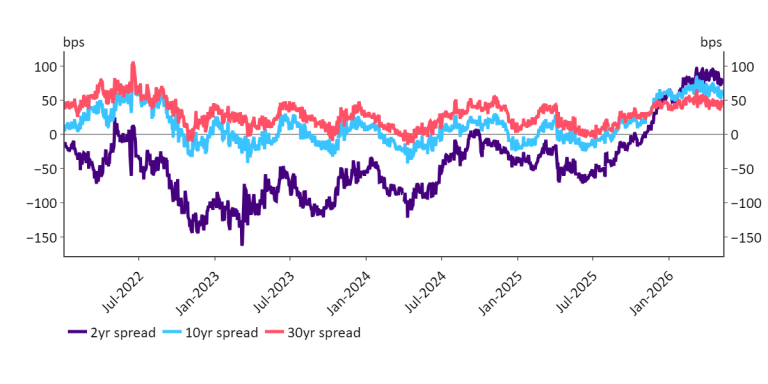

AGS continue to appeal to offshore investors given Australia’s strong sovereign credit profile, deep and liquid market, accessible hedging instruments and attractive yields relative to other advanced economies. Over the past year, AGS have become more compelling both in outright yield and relative spread terms, particularly compared with US Treasuries.

Charts 4 and 5 show that Australian sovereign yields have remained elevated relative to peers and that the yield differential with US Treasuries has widened, supporting increased offshore demand.

Chart 4. Sovereign 10-year yield comparisons

Source: Bloomberg.

Chart 5. Australia US sovereign yield spreads

Source: Bloomberg.

Dedollarisation of diversification?

The global repricing of sovereign risk over the past year has prompted many investors to rebalance towards higher-quality sovereign issuers, including Australia, while also more actively managing FX exposure.

The AOFM’s ongoing engagement with offshore investors confirms that investor demand is shifting toward greater diversification across both bond portfolios and currency exposures. While this has not resulted in broad-based reductions in US dollar allocations, portfolios are increasingly being rebalanced to include a larger share of non-USD assets.

Australian Government Securities—and AUD fixed income more broadly—have been a key beneficiary of this shift, supported by Australia’s strong economic fundamentals and the depth and liquidity of the AGS market.

Domestic Investors

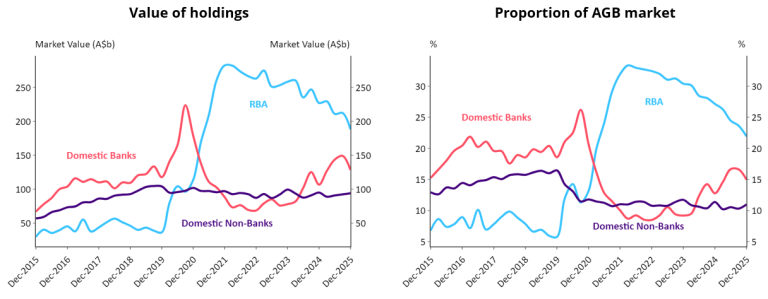

The domestic investor base comprises authorised deposit‑taking institutions (ADIs), superannuation funds, insurers and fund managers. Excluding the RBA, domestic investors hold just over 25 per cent of AGBs on issue. As of December 2025, the RBA held around 22 per cent of AGBs, down from a peak of nearly 35 per cent in 2022, and this share will continue to decline as bonds mature.

Domestic Bank holdings

ADI demand is supported by regulatory requirements to hold high quality liquid assets (HQLA). ADIs currently hold around 15 per cent of the AGB market, below the peak recorded in 2020. ADIs hold a larger share of the semi‑government bond market, reflecting higher yields, although demand for AGBs is expected to remain supported by declining exchange settlement balances and strong market liquidity.

Chart 6. Domestic Holdings of Australian Government Bonds

Source: ABS. AGBs are Treasury Bonds and Treasury Indexed Bonds.

Domestic non-bank holdings

Domestic non-bank holdings of AGBs have remained broadly stable over the past five years at around 10 per cent of AGBs outstanding. While AGBs remain a core portfolio holding for superannuation funds and insurers, much of the growth in domestic fixed income investment has flowed to semi government and non-government securities.

Investor trends from secondary turnover data

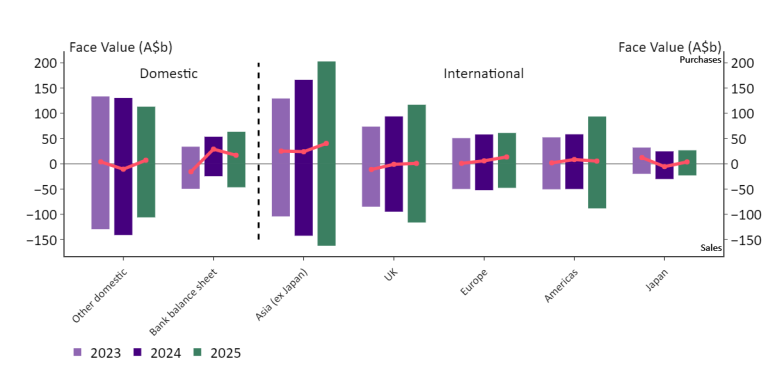

Secondary market turnover data indicate a sustained increase in offshore participation in the AGB market. Asia (excluding Japan) continues to account for the largest share of total turnover, with survey data indicating that AGB holdings in the region increased by around $50 billion in calendar 2025.

Investors from the Americas and the UK also recorded elevated levels of turnover, while European and Japanese activity remained broadly steady at lower levels relative to other regions.

Chart 7. Net investor turnover by region

Source: AOFM. Dates are in calendar years.

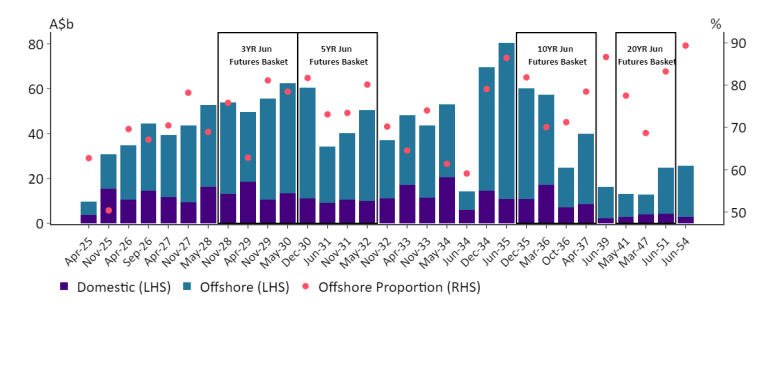

Chart 8 presents secondary market turnover by bond line for calendar 2025. Except for the matured November 2025 bond, non‑resident investors accounted for more than 50 per cent of turnover in each bond line.

Turnover was concentrated in the most liquid segments of the curve, particularly the 3‑year and 10‑year tenors, although activity was evident across the maturity spectrum, including in short‑dated and ultra‑long bonds. In the longest dated June 2054 bond, non‑resident investors comprised around 90 per cent of turnover.

Chart 8. Turnover by bond line ex-interbank (2025 calendar year)

Source: AOFM. This contains data for the 2025 calendar year.

While current turnover data do not classify offshore investors by type, AOFM engagement and participation in syndicated issuance confirms that offshore demand is well diversified.

New secondary turnover data

The AOFM will publish a new secondary market turnover dataset commencing with the March 2026 quarter. The dataset will include investor counterparty categories, providing substantially greater granularity and deeper insight into the composition and behaviour of the investor base. In addition, the new survey categories and reporting framework will be aligned across the AOFM and state government issuers, enhancing consistency and improving comparability across markets.

Outlook

Over the past year, investor demand for AGS has remained strong, particularly from offshore investors, supported by Australia’s strong sovereign credit profile, relatively attractive yields and the depth and liquidity of the AGS market. This demand has readily absorbed the additional supply associated with elevated issuance and the ongoing roll-off of the RBA’s bond holdings.

The AOFM strives to ensure the AGS market has a deep and diverse investor base. This diversity reduces the likelihood that a large proportion of investors will respond in the same way to market events, which supports the AOFM’s ability to undertake its issuance program, even in volatile market conditions.

While the AOFM does not directly control the composition of the investor base, given AGS are freely traded in competitive secondary markets, we have an important role in supporting diversity across investor types, sectors and geographies. This is achieved through a consistent and transparent issuance strategy, supported by extensive and ongoing investor engagement both domestically and internationally.

Maintaining a well-functioning 30 year Treasury Bond curve remains a central priority, underpinning the role of AGS as the risk-free benchmark across maturities. The AOFM will continue to issue into segments of the curve where demand is strongest, while balancing cost considerations with broader market development objectives, to support depth, liquidity and overall resilience of the AGS market.